PayPal Has Lost

Structural Decay and the $30 Billion Buyback Mirage

PayPal used to be the future of payments. Now it’s becoming the past.

Not overnight. Not dramatically. But steadily, structurally, and in a way that most people haven’t fully grasped yet — because PayPal is still enormous, still processing $1.79 trillion in payments a year, and still a household name. The problem isn’t that PayPal is small. The problem is that the two companies eating its lunch are growing at 38% and 33% respectively, while PayPal limps along at single digits.

That gap doesn’t close. It widens. Every single year.

This piece is about why. It’s about the layers of payment technology that most people never see, why PayPal’s architecture is fundamentally broken in a way that no CEO reshuffle can fix, and why the OpenAI deal everyone got excited about is, frankly, not that hot.

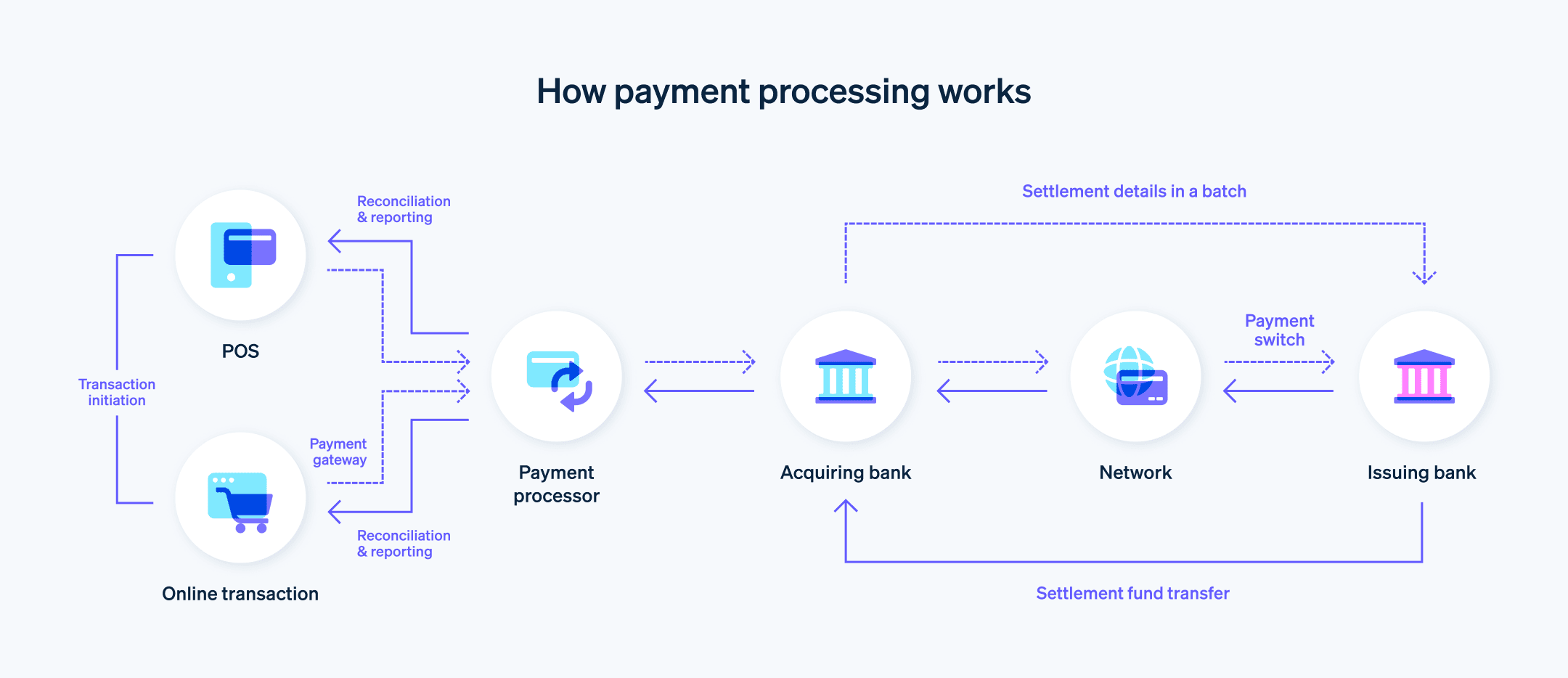

First, let’s talk about how payments actually work. Because most people have no idea.

When you tap your card at a shop or click “pay” online, it feels instantaneous. It isn’t. Behind that single transaction is a chain of handoffs that typically involves five to seven separate entities, each taking a cut, each adding latency, each adding risk.

Here’s the simplified version of what happens when you pay online:

You enter your card details. Those details get encrypted and sent to a payment gateway — the thing that captures and transmits your information securely. The gateway sends the transaction to a payment processor, which actually moves the money. The processor talks to an acquiring bank (the merchant’s bank), which talks to a card network (Visa or Mastercard), which talks to your issuing bank (the one that gave you the card). Your issuing bank approves or declines. The whole thing bounces back down the chain, and the merchant gets paid — usually within one to three business days

.

Now here’s where it gets interesting. Some companies sit at one layer of this stack. Some sit at two. A very small number of companies have built their own infrastructure across multiple layers simultaneously — owning the gateway, the processing, and in some cases direct connections to the card networks themselves.

That distinction — how deep into the stack you actually go — is the single most important thing to understand about payments. Because it determines your margins, your speed, your ability to innovate, and ultimately, your competitive position.

PayPal: A Frankenstein of M&A and “Sellotaped” Tech

PayPal’s problem isn’t that it’s bad at payments. It’s that it isn’t really one payments company. It’s five or six different payments companies that happen to share a logo.

There’s PayPal branded checkout — the legacy business, the one with the famous blue button. There’s Braintree — an unbranded payment processor that PayPal acquired in 2013 and that now handles a massive chunk of enterprise merchant volume. There’s Venmo — a peer-to-peer payments app that’s genuinely popular but monetises at a fraction of what PayPal checkout does. There’s Zettle — an in-person point-of-sale system. There’s Xoom — an international money transfer service. There’s Honey — a browser extension for coupon codes that PayPal bought for $4 billion and that has delivered, by most honest assessments, a fraction of that value.

Each of these products was built or acquired separately. Each has its own tech stack, its own product roadmap, its own way of thinking about the customer. And here’s the killer: they don’t talk to each other particularly well.

PayPal’s core problem isn’t just that it’s slow; it’s that it has seemingly lost the ability to build anything from scratch. PayPal’s internal engineering culture has become that of a holding company. Instead of a unified platform, they “sellotape” these acquisitions together with APIs that barely talk to one another.

The Margin Trap

PayPal’s branded checkout — the high-margin, high-take-rate business that actually makes the company profitable — is growing slowly. Braintree — the lower-margin, unbranded processing business — is growing fast, but it’s cannibalising PayPal’s take rate (the percentage fee PayPal earns on each transaction) in the process. PayPal’s blended take rate has been declining for years, because the business that’s growing fastest is the one that makes the least money per transaction.

This is the core tension. PayPal needs Braintree to compete with Stripe and Adyen at the merchant level. But every dollar of volume that moves through Braintree instead of PayPal branded checkout is a dollar that earns less. It’s a structural margin trap, and no amount of product innovation fixes it while the architecture stays the same.

In FY2025, TPV (Total Payment Volume — the total value of all transactions processed through the platform) slowed to 7%, reaching $1.79 trillion. But the real number to watch is the quarterly trajectory. Branded checkout TPV, the highest-margin part of the business, grew just 1% currency-neutral in Q4, down from 5% the quarter before. The deceleration is accelerating in the parts that matter most.

And the market noticed. PayPal reported FY2025 results this morning — February 3rd, 2026 — and the stock dropped 19% in a single session. The board fired CEO Alex Chriss the same day, citing execution that:

“was not in line with expectations.”

Revenue missed. EPS missed. And guidance for 2026 was described as “lackluster” by pretty much every analyst covering the stock. The company is now guiding for mid-single-digit EPS declines in 2026. This isn’t a company in transition. This is a company in trouble.

Technical Debt: The Silent Reckoning

Most investors understand financial debt, but technical debt is a more brutal beast. It is the invisible tax paid every time a company chooses a “quick fix” or an acquisition over a unified solution.

Unlike financial debt, where the interest rate is fixed, the “interest” on technical debt compounds based on complexity.

The Reality: Because PayPal has five separate checkout stacks, every time they want to add a single feature — like a new AI fraud layer — they have to build and test it five different times.

The Consequence: This is why R&D costs stay bloated while product velocity slows to a crawl. They aren’t innovating; they are spending billions just to make sure the sellotaped seams of 2013 acquisitions don’t burst under 2026’s volume.

When it takes PayPal 12 months to ship a feature that Adyen or Stripe can ship in two weeks, that is technical bankruptcy. You can fire the CEO, but you can’t fire the codebase.

Stripe: The Developer’s Payment Company

Stripe launched in 2010 with a deceptively simple pitch: make it easy for developers to accept payments online. A few lines of code and you’re live. No merchant account paperwork, no six-week onboarding, no phone calls to your bank.

That simplicity was, and still is, genuinely revolutionary. But Stripe’s real genius wasn’t the ease of setup. It was the depth of what it built underneath.

Stripe didn’t just build a payment gateway. It built a financial infrastructure platform. Payment processing, fraud detection, tax calculation, billing and subscriptions, identity verification, revenue recognition, treasury management — all in one place, all connected, all built from scratch on a single unified data architecture.

The numbers tell the story. In 2024, Stripe processed $1.4 trillion in total payment volume, up 38% year-on-year, equivalent to around 1.3% of global GDP. It’s now used by half of the Fortune 100, 80% of the Forbes Cloud 100, and 78% of the Forbes AI 50. And critically, Stripe was profitable in 2024 — a milestone that lets it reinvest earnings into R&D rather than burning cash to grow.

Stripe’s subscription billing product alone now runs at a $500 million annual revenue run rate, used by over 300,000 companies. That’s not a payments company anymore. That’s a financial software platform that happens to process payments too. The payments volume is almost a side effect of the broader platform.

The Collison brothers — Patrick and John, who founded Stripe — have consistently articulated a vision that goes well beyond “process card payments.” They’re building what they call the economic infrastructure of the internet. And increasingly, they actually are.

The Quiet Giant That Enterprise Payments Runs On

If Stripe is the developer darling, Adyen is the enterprise backbone. Founded in Amsterdam in 2006, Adyen took almost the opposite approach to Stripe: go directly after the biggest merchants in the world, and build a single unified platform that handles online, in-app, and in-store payments seamlessly.

The key technical advantage Adyen built is something called unified commerce — a single platform that processes payments across every channel a merchant operates, with a single view of the data. If you’re a global retailer with thousands of stores and a massive online presence, Adyen lets you see your entire payments operation in one place, optimise across channels, and reduce the number of payment providers you need to manage.

Adyen also holds direct acquiring licences in multiple countries, meaning it connects directly to local card networks and payment methods rather than routing through intermediaries. This gives it better authorisation rates, lower costs, and faster settlement — particularly for cross-border transactions.

Adyen’s processed volume reached €1.29 trillion in 2024, up 33% year-on-year headline — though it’s worth noting that strips out to 27% excluding a single large-volume customer (widely believed to be Cash App). Either number is impressive. Its profitability is genuinely stunning — EBITDA for 2024 was €992.3 million, representing a 50% EBITDA margin. That’s not fintech margins. That’s closer to a bank. And Adyen is growing faster than a bank by a considerable distance.

The client list tells you everything. Uber, Spotify, McDonald’s, H&M, Microsoft, Netflix — these are companies that need payments to work flawlessly, at scale, across dozens of countries simultaneously. They chose Adyen because it’s the only platform that can genuinely do that on a single stack.

Adyen famously refused to grow through M&A. Their 50% EBITDA margin is the reward for having zero technical debt. PayPal is a collection of silos; Adyen and Stripe are monoliths. In a race of speed, the monolith wins.

The TPV Race: Closer Than You Think

Here’s the number that should make PayPal nervous. In 2024:

PayPal: $1.79 trillion TPV (FY2025), growing 7% year-on-year — and decelerating.

Stripe: $1.4 trillion TPV (FY2024), growing 38% year-on-year.

Adyen: €1.29 trillion TPV (~$1.4 trillion, FY2024), growing 33% year-on-year (27% ex one large customer).

Do the maths. PayPal’s lead has already shrunk to roughly $400 billion. Stripe and Adyen are both growing at four to five times PayPal’s rate. At current trajectories, both overtake PayPal within two years. And PayPal’s growth rate is decelerating, not accelerating. Even if you use Adyen’s more conservative 27% ex-one-customer figure, it’s still nearly four times PayPal’s rate.

This isn’t a prediction. It’s arithmetic.

The difference between these companies isn’t just volume — it’s what volume means for the business. PayPal’s TPV is spread across a fragmented collection of products with wildly different margins. Stripe’s and Adyen’s TPV is concentrated on platforms built from the ground up for scale, with revenue streams stacking on top of each other.

Why the OpenAI Deal Isn’t as Hot as the Market Thinks

In October 2025, PayPal announced a partnership with OpenAI to embed its digital wallet into ChatGPT. Users will be able to discover products through ChatGPT and check out using PayPal. The stock jumped. The headlines were glowing. “PayPal is positioning itself for the agentic commerce era,” they said.

Here’s what they didn’t mention: Stripe had already done this. A month earlier.

Stripe announced it was helping OpenAI launch Instant Checkout in ChatGPT, with the feature co-developed using the Agentic Commerce Protocol — an open standard built by Stripe and OpenAI together. Stripe didn’t just partner with OpenAI. It co-built the infrastructure that ChatGPT commerce runs on. Stripe and OpenAI have partnered since 2023, when OpenAI began using Stripe Billing and Stripe Checkout for ChatGPT Plus subscriptions.

PayPal’s deal, by contrast, is to adopt a protocol that Stripe helped create and to plug its wallet into a system that Stripe already powers. It’s like celebrating that you’ve been allowed to use someone else’s railway.

There’s a deeper structural issue here too. The OpenAI deal positions PayPal as a wallet — a consumer-facing payment method that people use to check out. That’s the part of PayPal’s business that’s growing slowest and faces the most competition. Apple Pay, Google Pay, and now Link (Stripe’s one-click checkout product) are all eating into wallet share. The agentic commerce opportunity is real, but it’s primarily a merchant-facing infrastructure play — and that’s where Stripe and Adyen are stronger.

PayPal’s version of agentic commerce is: “People find things on ChatGPT and pay with PayPal.”

Stripe’s version is: “We built the checkout system, the payment processing, the fraud detection, and the open standard that the entire AI commerce layer runs on.”

One of these is a feature. The other is a platform.

The Wallet Future Is Less Profitable Than People Think

This brings us to the uncomfortable long-term truth about PayPal’s future.

PayPal’s highest-margin business is branded checkout — when merchants put the PayPal button on their site and customers click it. PayPal earns a premium take rate on these transactions because it’s adding value on both sides: trust for the buyer, conversion for the merchant.

But that premium is eroding. Merchants are increasingly sophisticated about payments. They know they’re paying more for PayPal checkout than they would for a raw card payment through Stripe or Adyen. And as alternatives improve — as Link, Apple Pay, and Google Pay become more seamless — the consumer-side trust advantage that PayPal once monopolised is shrinking.

The future PayPal is building towards — a digital wallet that lives inside AI chatbots, apps, and agentic commerce platforms — is fundamentally a lower-margin business than the one it’s leaving behind. A wallet is an intermediary layer. It adds convenience, but it doesn’t own the underlying infrastructure. The companies that own the infrastructure — the processors, the fraud systems, the checkout flows — capture more value.

PayPal is moving from owning the checkout to being one option in someone else’s checkout. That’s not growth. That’s margin compression with extra steps.

The $30 Billion Treadmill

While the tech stack decays, PayPal’s management has been running a sophisticated form of shareholder expropriation through Stock-Based Compensation (SBC).

PayPal touts its “robust” Free Cash Flow (FCF) as proof of health. But because SBC is a non-cash expense, it gets added back to the cash flow, creating a phantom profitability. Over the last decade or so (2016–2025), the numbers reveal a staggering wealth transfer from shareholders to employees and management:

Total Share Buybacks: ~$30.4 Billion

Total Stock-Based Compensation (SBC): ~$12.8 Billion

Net Capital for Actual Share Reduction: ~$17.6 Billion

Roughly 42% of every dollar spent on buybacks over the last ten years didn’t actually increase your ownership. It simply “mopped up” the dilution from the shares they gave away to keep the lights on.

In FY2025 alone, with $5B in buybacks and $1.6B in SBC, nearly a third of your “return” was actually just subsidising the payroll. At a $60 share price, PayPal issued approximately 26.7 million new shares to employees and management. You paid for the buyback, but you only felt the benefit of a fraction of it.

For the record Adyen has paid around €135m in SBC over the last decade. For every €1 Adyen has spent on rewarding employees with stock, PayPal has spent roughly €95. And what exactly have you got for that money?

The Verdict on SBC

The hubris lies in the Non-GAAP reporting. If PayPal pays a developer $200k in cash, it’s an expense. If they pay that same developer $100k in cash and $100k in stock, PayPal claims their “Adjusted” profit is $100k higher. But the economic reality is identical: $200k of value left the company.

PayPal is buying back the furniture to pay the rent. They are transferring wealth from the balance sheet to an employee and management base struggling under the weight of a decade of technical debt.

So What Does This Actually Mean?

Stripe and Adyen are not just growing faster than PayPal. They’re growing faster while building deeper, more defensible businesses. Stripe is becoming the financial operating system for the internet. Adyen is becoming the unified commerce layer for the world’s largest enterprises. PayPal is trying to be a wallet in a world where wallets are becoming commoditised.

The OpenAI deal bought PayPal a few weeks of positive headlines. It didn’t change the fundamental trajectory.

PayPal isn’t dying. It’s still processing $1.79 trillion a year. It still has 439 million active accounts. It still has brand recognition that Stripe and Adyen can’t match in consumer markets.

But brand recognition doesn’t compound. Infrastructure does. And right now, the companies building the infrastructure are the ones that will own the next decade of payments.

The market got a brutal reminder of this today. PayPal’s stock dropped 19% in a single session. The CEO was fired. Guidance was slashed. And somewhere in Amsterdam and San Francisco, the teams at Adyen and Stripe didn’t even flinch.

Watch Stripe. Watch Adyen. And watch PayPal figure out whether it’s a payments company or a wallet app — because it can’t be both, and the market is forcing the choice.

This post is sponsored by Trading 212.

If you’re looking for a new platform to start or continue your investment journey, you should check out Trading 212. You can sign up using the code “FTSE” to get a free share worth up to £100 or just click on this link;

https://www.trading212.com/Jdsfj/FTSE

Terms Apply. All content is for informational purposes only and is not investment advice. Trading 212 is a platform for investing, and as with any investment, your capital is at risk.